A Mutual funds let you pool your money with other investors to “mutually” buy stocks, bonds, and other investments. Mutual funds are managed by professional fund managers who make investment decisions on behalf of the investors.

SIP allows you to invest a fixed amount periodically (monthly, quarterly, etc.), making it a disciplined way to invest.

Investing a large, one-time amount in a mutual fund scheme.

A type of mutual fund offering tax benefits under Section 80C of the Income Tax Act.

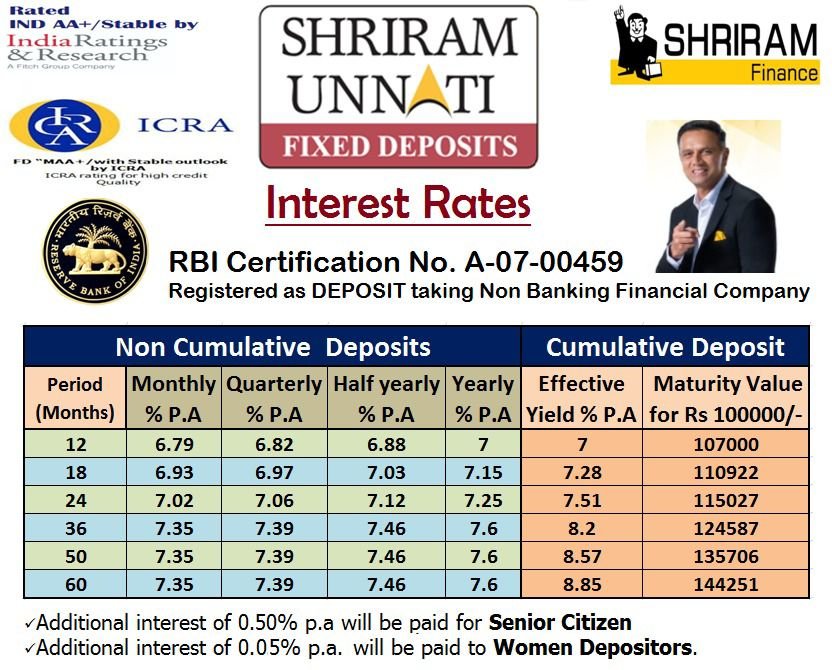

A Fixed Deposit (FD) is a popular investment tool offered by banks and financial institutions, where you deposit a lump sum amount for a fixed tenure at a predetermined interest rate. It is considered one of the safest investment options as it provides assured returns and is not influenced by market fluctuations.

Whether you’re planning for your child’s education, your retirement, or simply looking to grow your savings, Shriram unnati fixed Deposit provides a secure and reliable pathway to financial success.

WhatsApp us